U.S. trade and immigration policies are reshaping the competitive environment and labor market for American energy companies. While many analyses of the new administration’s policy regime have explored tariffs or immigration separately, none has modeled their combined effects. Using our global computable general equilibrium (CGE) model, we assessed the long-run economic effects of these policies in tandem—effects both on the U.S. national economy and specific U.S. industries.

There is a long-standing consensus among economists about the adverse aggregate effects of increasing tariffs and reducing labor supply. Over time, tariffs introduce inefficiencies by raising the costs of goods and reducing the competition faced by domestic businesses. Reduced immigration limits the overall number of available workers, raising labor costs for businesses and, ultimately, prices for consumers.

Such adverse aggregate-level outcomes, however, do not necessarily hold for all industries. When it comes to the U.S. oil and gas industry, our analysis shows a clear picture: Trump administration efforts to reduce the number of undocumented workers and raise tariff rates will likely combine to reinforce the domestic competitiveness of U.S. oil and gas, boost domestic oil and gas manufacturing, and expand opportunities for U.S.-based suppliers and workers.

For oil and gas companies, service providers, and manufacturers, the coming years represent an opportunity to grow and visibly consolidate their contribution to domestic energy and economic security. For community and state leaders, the challenge and opportunity is to develop reliable hubs of skilled domestic labor attractive to oil and gas employers. Workforce development, vocational training, and targeted incentives could bolster the number of people entering the workforce and draw investment to geographic areas prepared to respond.

U.S. Oil and Gas Set to Benefit

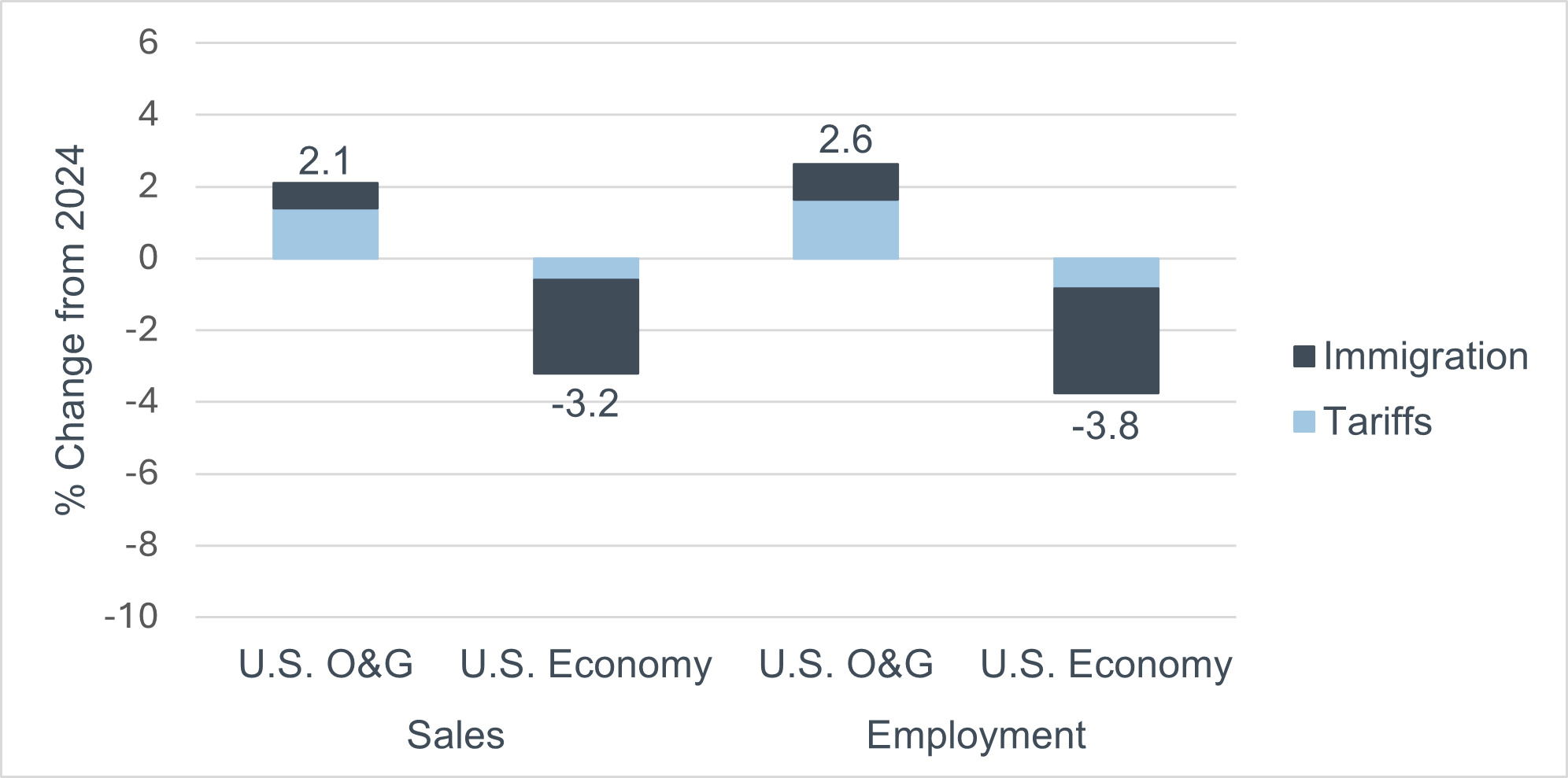

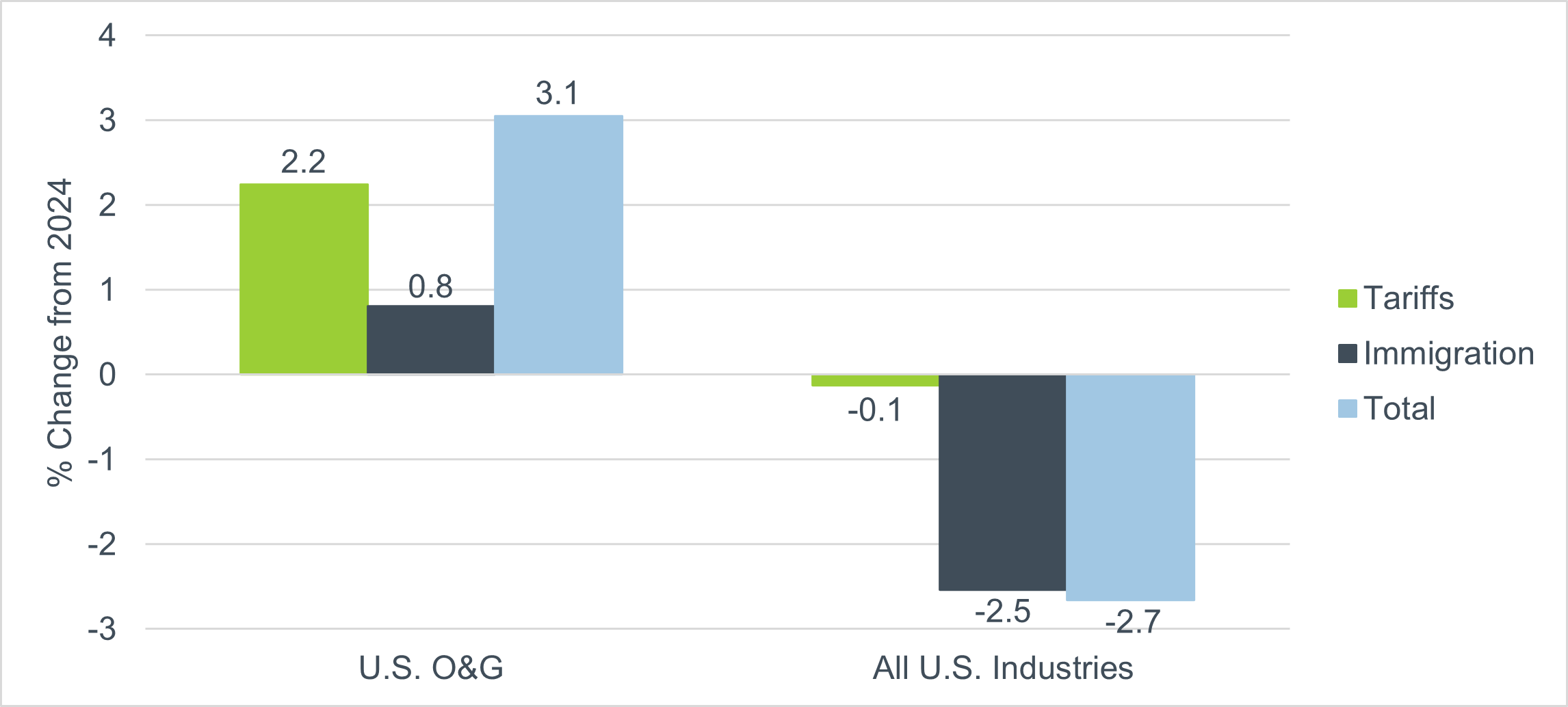

Our modeling shows the U.S. oil and gas industry is set to expand as a result of these policy changes, leading to significant increases in domestic spending. Annual output is projected to rise by $7.6 billion (+2.1 percent), accompanied by an increase of 3,200 jobs (+2.6 percent). This growth will generate an additional $4.1 billion (+3.1 percent) in annual purchases of U.S.-made goods and services.

The following chart summarizes the net effect of Trump administration policy changes on sales and employment in the oil and gas industry, breaking down the anticipated impacts in terms of immigration policy effects—assumed to result in a reduction of approximately 4.5 percent in the U.S. low-skilled labor supply by 2028—and tariff policy effects.

Our analysis shows that as imported inputs become less cost-competitive, oil and gas companies will be able to expand supplier networks and source more domestically, reducing dependency on overseas markets and supporting American manufacturing.

In this new policy landscape, oil and gas companies have a chance to broaden supplier networks, expand investment in U.S. goods and skills, and diversify their procurement within the United States. For U.S. regions, especially those with advanced manufacturing or skilled labor bases, this is a moment to attract new energy-related investment. Targeted policy tools such as tax credits, infrastructure upgrades, and workforce training programs could ensure these benefits are widely distributed. Economic development officials at the regional, state, or municipal level have an immediate opportunity to identify where these gains are most likely to materialize and ensure that suppliers, workforce programs, and infrastructure are ready to support them.

Local Supply Chain Participation Is Geographically Uneven, But Growing

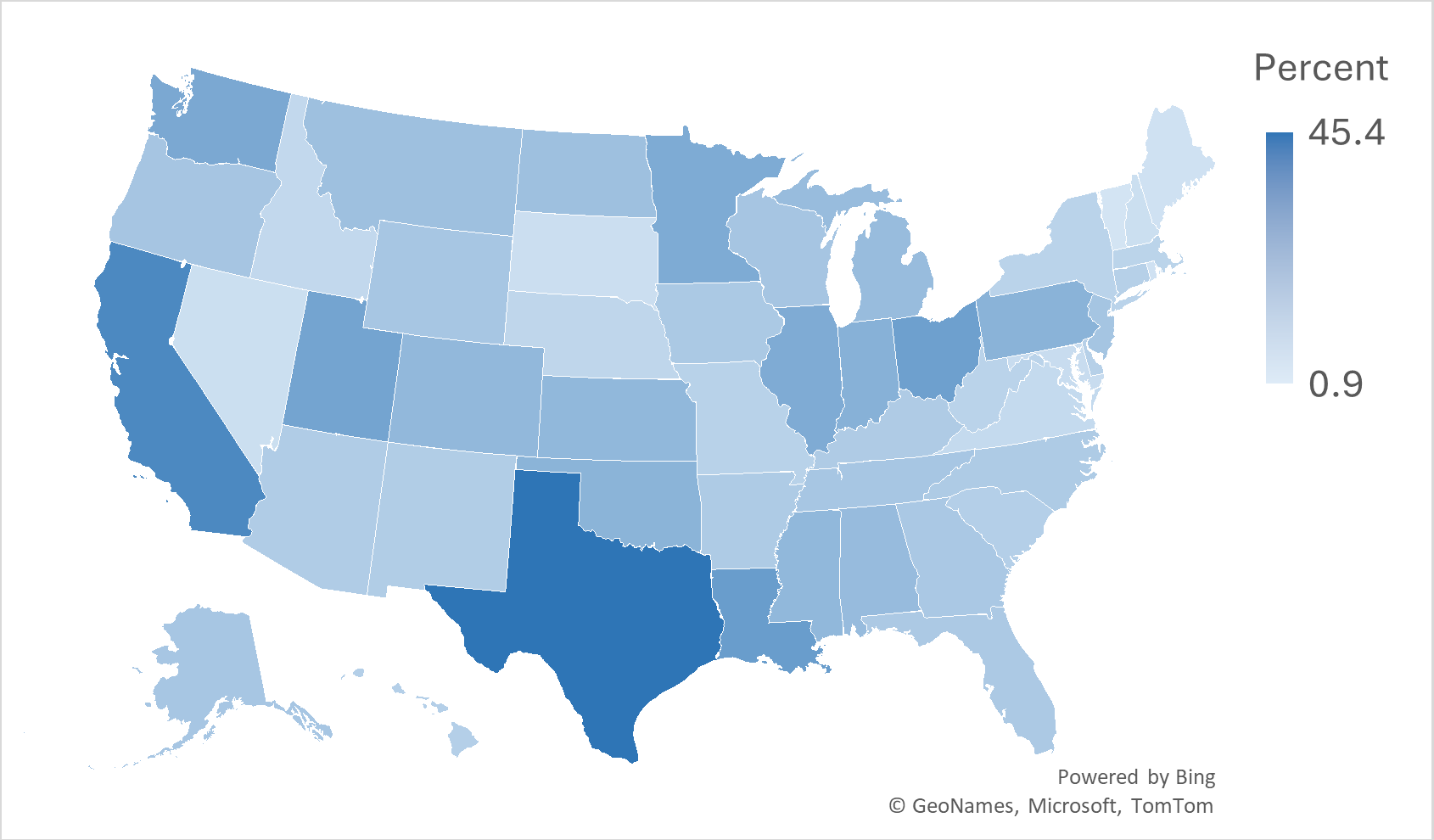

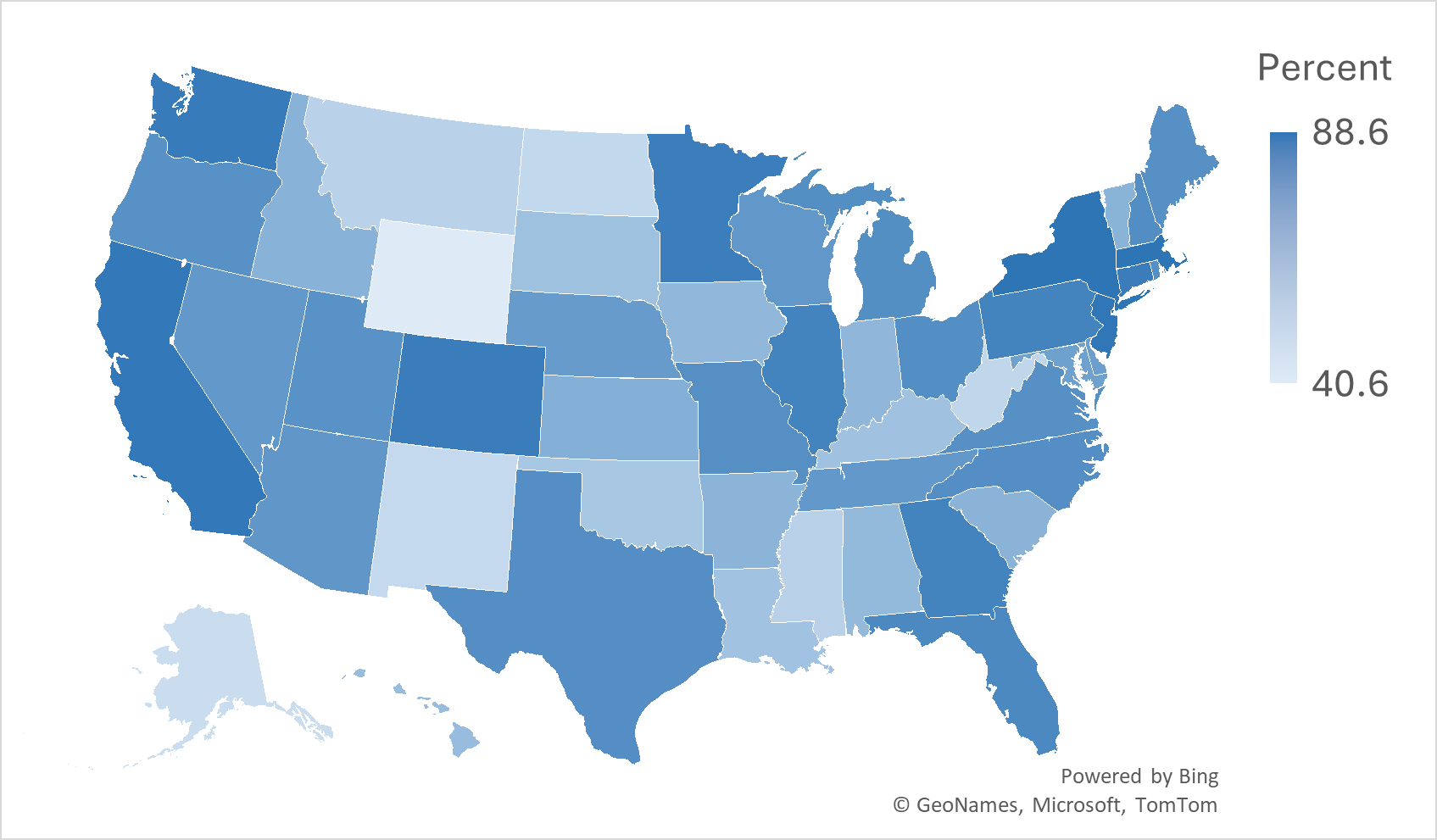

As the oil and gas industry expands its spending and investment in the US, the next question becomes where those opportunities will take root and how the benefits of growth can be more geographically distributed. Our state-level analysis of 2023 data from the IMPLAN Group shows that most oil and gas manufacturing purchases are concentrated in Texas and California, while service-based spending is distributed more evenly across the United States. As domestic spending increases, there is an opportunity to strengthen and expand supply chains across a wider set of states, creating a more competitive, resilient, and community-connected U.S. oil and gas industry.

Geographically diversifying supply chains would benefit U.S. energy companies in several ways. A broader manufacturing base would lower costs over time by increasing supplier competition, shortening transport distances, and reducing socioeconomic risk through stronger local engagement. Companies that source more broadly within the United States also stand to gain a greater social license to operate, as new investments translate into visible benefits for more communities.

With this significant scope for U.S. manufacturing diversification, local and regional authorities have a clear opportunity to position their workforces and industrial bases to participate in this growing national market. According to recent research, approximately 47 million people (about 14 percent of the U.S. population) live within 1 mile of fossil fuel energy infrastructure. These communities represent a ready network of potential partners and beneficiaries for expanded sourcing by a growing oil and gas industry; energy companies looking to extend their supply bases beyond traditional hubs are likely to find supportive partners among the states and municipalities positioned to host new facilities, train skilled workers, and capture the benefits of policy-driven domestic investment.

Moving Forward

By strengthening its local supply chains and investing in U.S. skills and manufacturing, the energy industry can enhance its resilience, competitiveness, and contribution to national growth. We will be monitoring the emerging policy and market environments to understand what they mean for companies, governments, and communities across the United States, helping our partners turn these insights into actionable strategies for smarter planning, better risk mitigation, and long-term value creation.

Methodological Note

DAI provides advanced analytics to help our clients anticipate change, adapt strategies, and capture growth opportunities, including through site- and project-specific economic analysis, workforce solutions, and local economic development plans for companies and governments.

The model used for this analysis is an extension of version 7 of the GTAP Standard Model (Corong, et al., 2017), run using GEMPACK software. The extension, GTAP-E (Corong, 2023), modifies the Standard Model to accurately represent the production, consumption, and trade of energy in the global economy. The CGE model estimates the changes in the economy’s steady-state level due to the tariff and immigration policies. It does not explicitly model the passage of time. The conventional definition of the term “long-run” when interpreting results from this type of model is “five or more years” from occurrence of the policy change(s). Global tariff policies as of August 11, 2025 are modeled for this analysis.

For more information on the assumptions underlying this analysis, contact Luke Kozumbo.